A note about independent sales representatives

As an independent sales representative (eg, Avon), it’s tempting to think of the commission element as being your “income” for tax purposes. After all, that’s the only bit you get to keep.

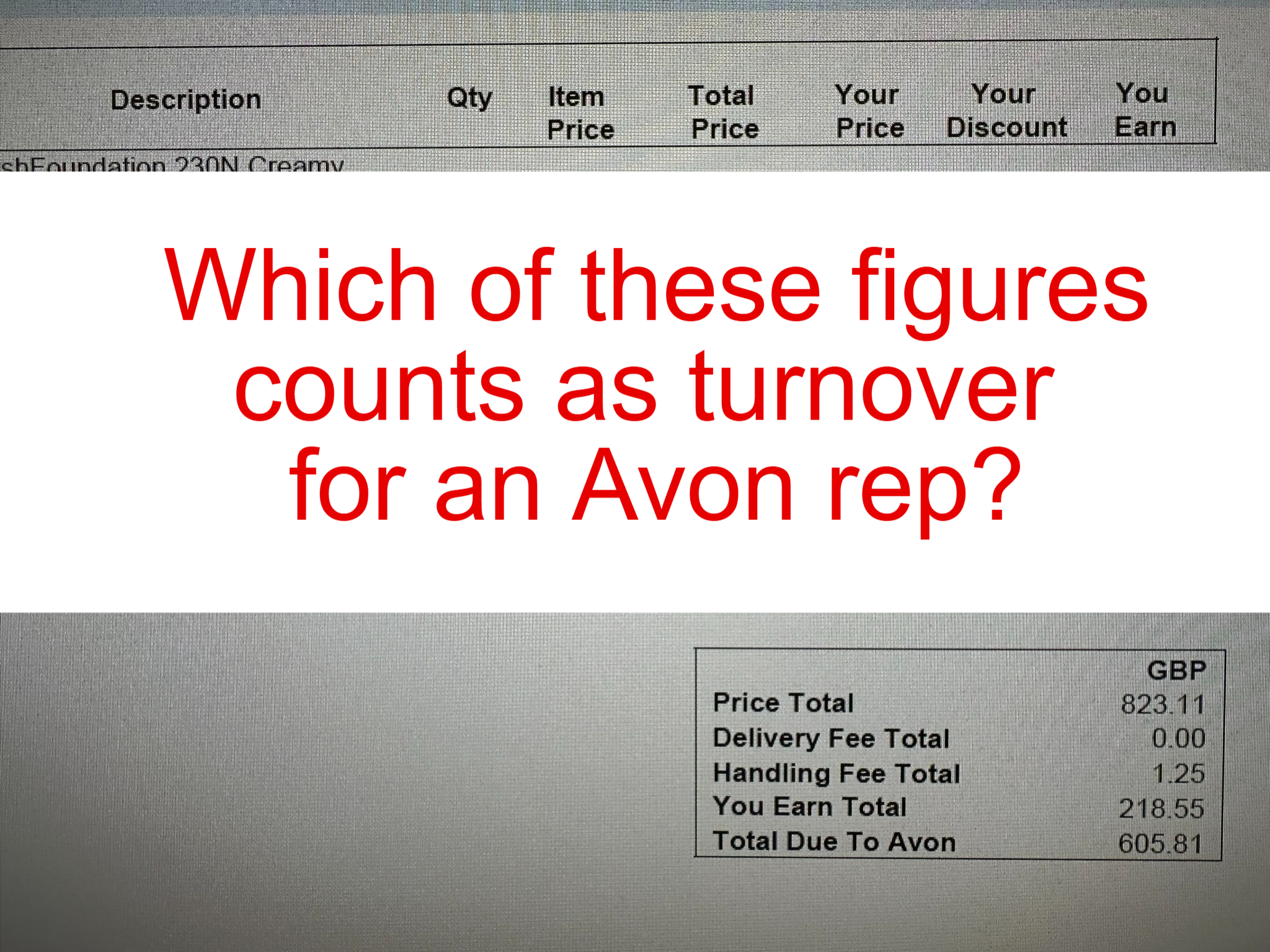

But the way it’s viewed for tax purposes, is that you’re buying the products from Avon at 70-100% of the selling price, and then collecting the full price from your customers. The figure you need to put in the turnover box on your tax return is the amount you collect from your customers, not the commission.

You might thinking, well, what difference does that make? If the goods I’m buying from Avon are an allowable expense for tax purposes, surely it doesn’t matter whether I report £900 commission in the turnover box on my tax return, or show my turnover as £3,000 and claim the £2,100 I paid Avon as an expense?

Where it makes a difference, is in the trading allowance.

HMRC allow you to earn up to £1,000 without having to register as self-employed or complete a tax return. This tax-free amount is known as the trading allowance.

But that’s £1,000 of income, not profit, so you can’t deduct any expenses.

Using the figures above, if your commission is only £900, it’s easy to think that you don’t have to register with HMRC because the income you get to keep is less than £1,000.

But that’s not how HMRC sees it. By signing the Avon Representative Agreement, you agreed to promote and sell Avon products “on your own account”, acting as a “principal” (not agent). Which means that HMRC consider your turnover to be the full price of the products you’ve sold to your customers.

So, if the amount you collect from your customers over the course of a year is more than £1,000, you have to register as self-employed and complete a tax return.

But it gets worse. Not only do you have to declare the full selling price as your turnover, but you’re also unlikely to benefit from the other way that the trading allowance can be used – as a fixed deduction.

A self-employed person registered with HMRC can choose to deduct a fixed amount of £1,000 from their income instead of calculating actual expenses. Except, chances are, you’ve already paid over £1,000 to Avon alone just to buy the products you sold. Which means you can’t take advantage of this simplification either.

Even if you’re only left with pocket money after you’ve deducted all the other costs of running an Avon business – demo products, brochures, bags, postage and handling from Avon, mileage to deliver the products to your customers, and your accountant’s fees (if you use one) – you’ll need to keep a full record of all your expenses.

In summary:

- If you’re an independent sales representative, check the terms of your representative agreement. If it states that you are a “principal”, the figure you need to put in the turnover box on your self-employed tax return is the amount you collect from your customers. The cost of the goods gets shown as an expense.

- If the amount you collect from your customers over the course of a year is more than £1,000, you will have to register as self-employed and complete a tax return.

- If the total amount you paid to the company you represent plus the other costs of running your business exceed £1,000, you’ll need to keep a full detailed record of all your expenses.

For more bookkeeping and tax tips, follow Springreach Training & Coaching on social media or visit springreach.co.uk.